歡迎登入(帳密皆為學號)

請參與本學期(112-2)實務專題發表的大三同學,務必注意相關時程!

報名連結:https://forms.gle/

報名連結:https://forms.gle/

首場日期:3月29日(星期五)

首場日期:3月29日(星期五)

活動時間:晚上8點 - 9點

活動時間:晚上8點 - 9點

公告報名期限:113年3月20日至4月21日止

🚀AI數據分析師養成班第一梯次,12/27日報名截止、12/29開課。

https://bit.ly/47HITJF

✅資格:15歲至29歲本國籍待業者(加保工會者可報名)。

✅費用:免費(訓前預付10,000元,訓後投保即可補助1萬元)

專題得獎小組,頒發每人獎狀乙只並發放獎學金,以資鼓勵。

特優1,000元,優等800元,佳作500元。

※請得獎小組推派一員填寫匯款資料⇒https://forms.gle/5msGkaJzuakdmUjt6

並準備銀行或郵局存摺影本mail至fmchung@nkust.edu.tw,請於112.6.17前填覆!

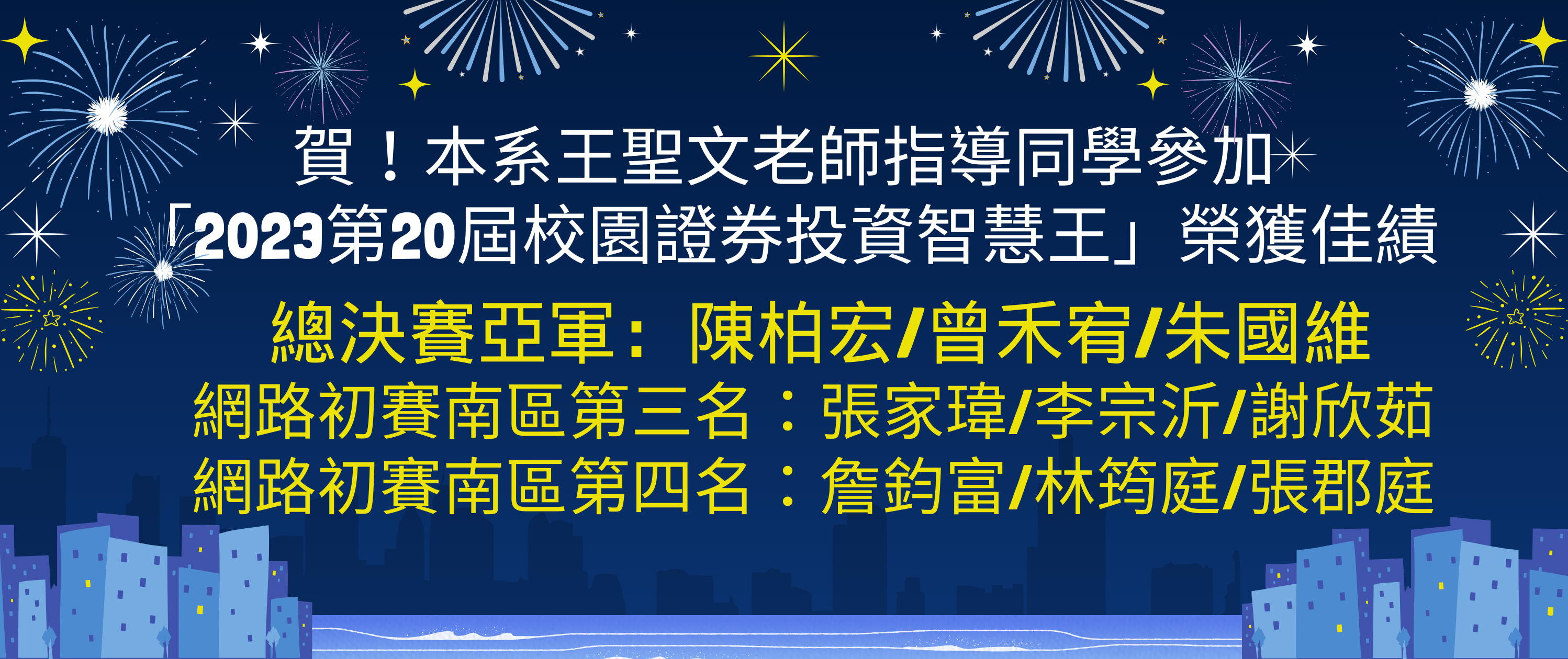

狂賀!!本系陳柏宏、曾禾宥、朱國維同學榮獲總決賽亞軍!

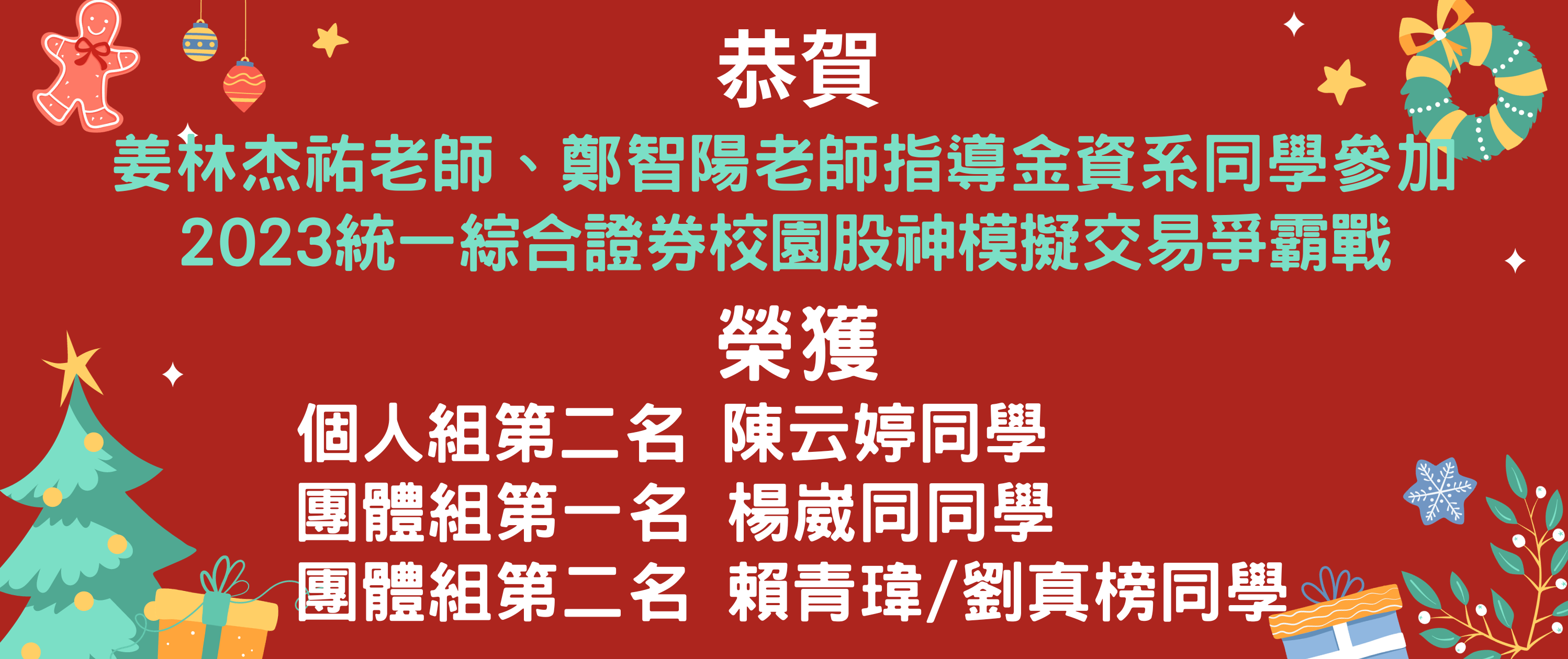

狂賀!!本系洪偉哲、曾宣瑋、張家瑋同學榮獲總決賽亞軍!